Wage Cycle Suggests Fed Tightening Cycle Not Over

- May 5, 2023

- 2 min read

The wage cycle is a critical factor in the scale and length of the Fed tightening cycle. Based on the current wage data, history says the tightening cycle has yet to reach its peak rate, and the duration of the higher official rate cycle could extend much farther than the markets expect.

The thinking behind the Fed hiking rates to break the inflation cycle is straightforward: lift rates to a prohibitive high enough level that curtails or breaks the willingness to borrow and spend. Each tightening cycle is different, and the scale and length often depend on wage and income growth.

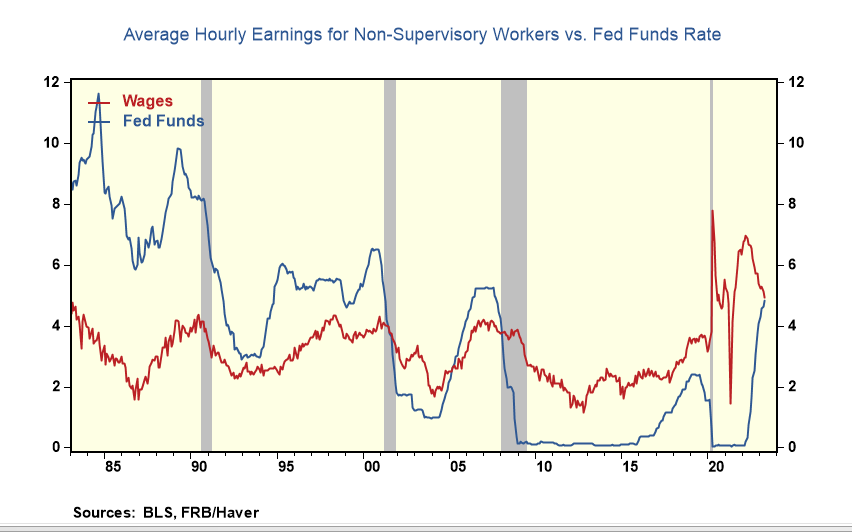

One traditional way to determine if higher rates are prohibitively high is to compare them to inflation. That helps determine the real borrowing costs for businesses since the price is what firms get for their products and services. Yet, to measure the real borrowing costs for consumers, one needs to compare interest rates to wages since the latter is the worker's price.

In April, and for the first time since the Fed started to raise official rates in March 2022, the gap between Fed funds and wage growth was closed. That's the good news. The bad news is that the tightening cycles of the late 80s, 90s, and mid-2000s ended when official rates were several hundred basis points over the wage growth. So history would say the Fed tightening cycle is far from over, and the April wage and jobs data lends credence to that view.

Still, policymakers may pause and gauge the lagged effects from the scale of the tightening to date. Lagged effects from monetary tightening are adverse and build over time. Still, the overall stance of monetary policy must be tight or restrictive for them to generate the negative economic and financial results policymakers want to achieve.

Up to this point, the policy stance shifted from less accommodative to neutral and could be headed into a tightening phase in the coming months and quarters if policymakers hike more. That helps to explain why cyclical sectors ( motor vehicle sales in April were the highest in nearly two years, and housing activity has perked up) showed renewed momentum. More rate hikes will be needed to break that momentum.

Comments