No Way: Financial Fear Equal To That of 9/11

- Joe Carson

- Mar 1, 2020

- 4 min read

Updated: Mar 6, 2020

Uncertainty surrounding the global economic and financial implications of the fast spreading coronavirus was the catalyst for sharp drop in the US equity market during the last week of February. Yet, the speed and the scale of the decline were also influenced by how far finance had separated from the economy.

Stock Market’s Sharp Drop

The sharp decline in the equity market was both historic and unusual. In a span of 5 trading days, the S&P 500 index dropped 11.5%, one of the largest single week declines on record. And what is also unusual about the decline was that there was no “hard” evidence of any disruption or decline in the domestic economy.

Yet, to be fair equity investors were reacting to a growing number of companies that have indicated Q1 earnings will fall below their initial guidance due to weakness in overseas economies (especially China) as well as the disruption to global travel and supply chains.

To illustrate how substantial last week’s plunge in the equity market was it nearly matched the 11.6% decline in the S&P 500 index for the first week of trading that followed the horrific events of 9/11. Now that comparison by no means is trying to compare the financial fears of last week with the horrific tragedy of 9/11. 9/11 stands alone in American history as one of the most tragic events ever, as it changed a city and a nation far beyond what any of the numbers say.

Yet, the comparison was offered only to suggest that given the speed and scale of the decline other factors beyond the coronavirus could have played a large role as well.

One possible explanations could be how far finance (equity markets) had separated from the real economy, as well as how monetary policy in recent years has made investors rely on cheap money and forget about the risks of equity investing. Here are a few examples.

Finance vs. Economy

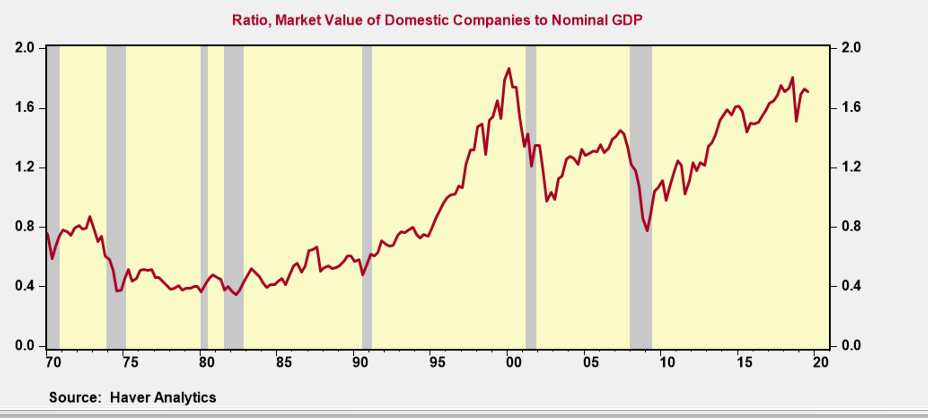

First, operating profits for US companies have not increased for 5 consecutive years, and yet the S&P 500 had climbed over 60% during that period. Also, the market value of domestic companies to nominal GDP----a ratio that is often used to determine if the equity market is undervalued or overvalued relative to a historic average---stood at an estimated 1.85x at the end of 2019, matching the record high of 2000.

The run-up in equity prices and valuations over the past several years was fueled by easy money, along with the promise of low rates for the foreseeable future. As such, investors viewed stocks as low risks, with many professional investment advisors going as far as arguing that they “didn’t see any alternatives to stocks”.

Second, coronavirus puts “risk” back into investing, something that has been absent in recent years as policymakers have responded to every “illness” or setback in the markets with the promise of support. Also, the new “risk” factor (coronavirus) has an uncertain life and unquantifiable consequences, and cannot be “cured” by more easy money.

Third, the fast run-up in equity prices for so many companies, even for those continuing to report operating losses, forced equity analysts to keep raising their price target to stay relevant, or come up with new ideas or ways to justify higher valuations.

One analyst came up with a new idea on how to value Tesla, a manufacturer of electric cars. The analyst offered various scenarios. The base case price target called for nearly a 40% price drop from the stock’s current price (“reflecting an unfavorable risk-reward skew”), whereas the bull case price target was 50% higher, based on 2030 volume and operating margin.

Tesla went public in 2010 and has yet to have one profitable year. Nonetheless, in early February Tesla stock price hit a record $969, a fourfold increase since October---just one example of how finance became separated from current economic conditions. At the end of February Tesla’s share price stood at $668.

Where Do We Go From Here?

Missteps in policy decisions created a large gap between finance and the economy. Fed’s policies of low rates ended up inflating finance over economy much more so that it had in success of hitting its price stability target. The fact that a market correction occurred was not a surprise, but the catalyst was.

It would be wise for policymakers to let the re-balancing between finance and the economy run its course, and also let the financial system re-price risk in a natural way. Yet, “politics” may force the Fed to play a role not well suited for traditional monetary policy.

Investors must stay focused on the behavior response of consumers and business to the plunge in equity prices and coronavirus. Each of the past two recessions were caused by a sharp plunge in asset prices, so the loss of household wealth and liquidity does raise the odds of a bad outcome. Consumer confidence for now may be shaken more by the speed of the decline than the scale.

Coronavirus has the potential to be even more disruptive. That’s because all of the unknowns about the new virus could compel people and business to become idle, and when the flow of business activity slows or stops so does profits (and soon jobs) in a number of industries.

Perhaps the biggest worry nowadays is that businesses are operating with a record debt load. Even though borrowing costs are exceptionally low, businesses still need to generate revenue to pay its debt obligations (as well as its’ workers). Small businesses might be the most vulnerable since they don’t have financial resources of large firms, and few, if any, could survive a few weeks of little or no sales. More than one-third of small firms are already burdened with high debt according to the Small Business Credit Survey conducted by the Federal Reserve Banks in 2019.

With the global coronavirus situation still fluid investors should be prepared for more disruption to business with the "big" risk that the disruptions spillover to the labor markets, if not lead to a number of corporate debt downgrades and a rise in business bankruptcies at some point.

Comments