The Truth About The Current Inflation Cycle

- Joe Carson

- Apr 13, 2022

- 2 min read

Although a few presumably temporary factors have lifted reported inflation well above expectations, it is also true that some elements made it look less troublesome. So what is the truth about the current inflation cycle?

The Bureau of Labor Statistics (BLS) provides special aggregate price series that remove the noise, or an underestimate from these factors. For example, BLS published a series of CPI less food, energy, shelter, and used car and truck prices. This series removes the recent temporary spikes in food and energy prices linked to the Russian invasion of Ukraine. It also removes the massive spike in used vehicle prices associated with supply bottlenecks owing to the pandemic. On the flip side, it removes the controversial shelter component that no longer captures house price inflation.

In April, BLS reported this price series increased by 0.6%

month-on-month, matching the gain in March and twice that of the 0.3% gain in the so-called core inflation series. This price series has increased by 5.8% in the past year, matching the highest rate recorded in the prior 40 years.

The surge in this price series also represents a significant milestone. It breaks four decades of lower peak-to-peak consumer inflation rates in the business cycle. Business cycles have shown that there is a cycle in prices. Yet, up until the Volcker era, the peak-to-peak was progressively higher. And after the Volcker era, the peak-to-peak inflation rate has been progressively lower or stable.

Also, the surge in this price series shows that the current inflation cycle is not a "blip." On the contrary, it is widespread and more embedded in the decisions and expectations of consumers and businesses.

It is unclear if the current generation of policymakers is aware of the price cycles in the business cycle or how pipeline pressures feed into product prices. For example, the producer price report showed significant increases at all three processing stages in April. It's unlikely that monetary policy can break these price increases with modest increases in policy rates.

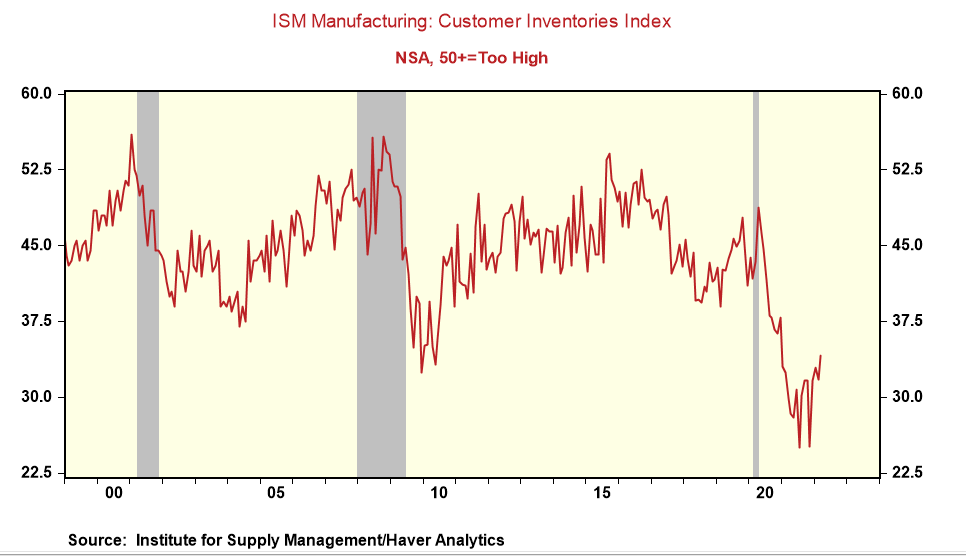

Companies need materials and supplies to protect production schedules. Notably, the April survey of manufacturers from the Institute for Supply Management showed that customer inventories are near record lows. As a result, it would take exceptionally high-interest rates to force companies to pull back on the inventory investment needed to sustain production.

Although policymakers have yet to list easy money as one of the causes of the current inflation cycle, it plans to make money much more costly to break the cycle. Yet, how far are policymakers willing to take official rates to reverse the price cycle?

The current official rate projections of policymakers show a peak fed funds rate of 2.8% in 2023, less than half the inflation rate, excluding the unique factors. Never has an inflation cycle been reversed or broken without policy rates moving above the reported inflation rate. Investors will soon need to confront whether the higher cyclical peak inflation rate is a one-time occurrence or a sustained shift to higher rates? I bet its the latter because the current generation of policymakers is unaware of how price cycles start and end,

Comments