The Next Catalyst For Inflation: Significant and Persistent Increases In Labor Costs

- Joe Carson

- Dec 12, 2021

- 3 min read

Significant and persistent increases in labor costs could be the next big surprise in the inflation cycle. My research found that the most reliable signal on the labor market is the monthly change in the civilian unemployment rate. Since the spring, the record drop in the civilian unemployment rate indicates that the labor markets have far passed the point of demand and supply balance. That will force companies to continue increasing pay to maintain workers and attract new ones.

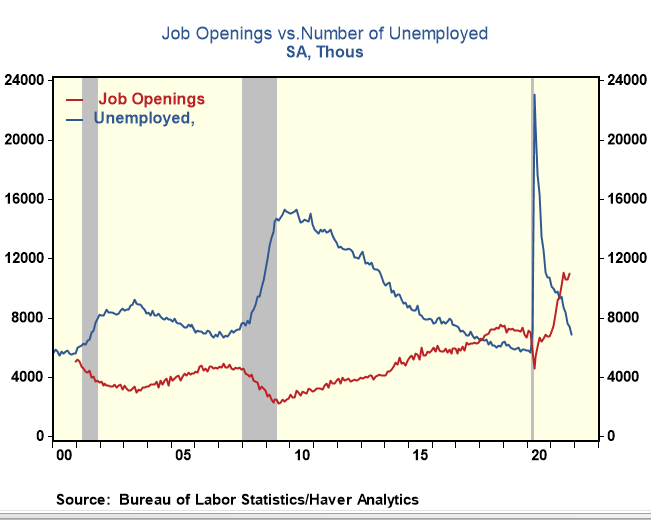

November's unemployment rate of 4.2% is 1.8 percentage points below March. Over that period, the jobless rate recorded monthly declines of 0.4 percentage points or more three times. Monthly drops in the jobless rate of 0.4 percentage points or more are rare. It's even rarer to occur when the jobless rate is at or below 6%. It happened four times in the past 50 years, and three of those occurred since March. Also, the last time the jobless rate starting at 6% fell as much as it did in 2021 was 1950---over 70 years ago.

Press reports indicate that companies plan the most significant wage increases in 2022 in over a decade. Yet, with job openings at 11 million and exceeding the number of unemployed by 4 million, the odds are high that wage costs will surprise as much on the upside as commodity and freight costs did in 2021.

A few months ago, large companies, such as Walmart, Costco, and Amazon, announced pay increases and significant pay incentives for workers to stay with the firm in 2022. At those announcements, the jobless rate was around 5%; there is even more pressure now, with the jobless rate approaching 4%. The most severe pressure is likely to be felt in smaller companies (100 or fewer workers) since losing a handful of workers will force others to work longer hours, demanding more pay in the process.

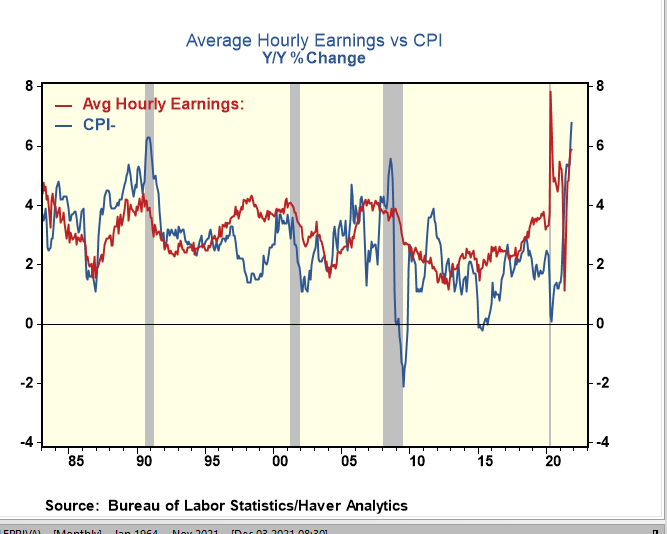

Average hourly earnings have increased 5.9% in the past year but still, trail inflation by 100 basis points. Workers want more. Wage increases have not exceeded consumer price inflation for an extended period since the late 1990s. But, the balance of power between labor and employers has shifted, and faster wage increases are in store for 2022.

So far, the current inflation cycle has been more significant and broader than expected. Despite its scale and persistency, many are forecasting an end to the inflation cycle, citing stable to lower oil prices and easing freight and shipping costs. Yet, that optimistic view contradicts the lessons learned from the 1970s inflation cycles and the political trade-off at the Fed of fighting inflation at the expense of jobs and wages.

Supply-side factors, impacting a wide range of agricultural and industrial commodities, sparked the 1970s inflation cycle. That is similar to what sparked the current inflation cycle. But, years of easy money and expansive fiscal policy extended the 1970s inflation cycle.

Fed policy nowadays is more accommodative than the entire decade of the 1970s. At the same time, the federal government appropriated a record $5.6 trillion in spending (roughly 25% of GDP) over the past two years, with the White House hoping Congress will pass another round of stimulus before year-end. In the 1970s, fiscal stimulus was a fraction of that.

With that monetary and fiscal accommodation scale, it makes more sense to look for reasons the inflation cycle will live instead of dying on its own. Surprised by the 2021 inflation cycle, policymakers and many analysts appear to be making the same mistake by ignoring the factors that could sustain the inflation cycle in 2022.

Comments