The Big Risk in 2023 For the Fed & Investors---Slowdown in Inflation Proves To Be "Transitory"

- Joe Carson

- Nov 27, 2022

- 3 min read

Federal Reserve policymakers are considering implementing smaller rate hikes, acknowledging the lagged effects of previous rate hikes and better news on inflation. Investors have been running with this bullish view that the apparent slowdown in core inflation, along with declines in commodity prices, changes the inflation outlook so that policymakers would scale back and possibly end their rate-hiking experiment in early 2023.

The rally in equities has been impressive. From the low on September 30, the Dow Jones is up 20%. If the equity market follows the historical pattern between the second and third year of presidential terms, there is much more to go. The average gain in the Dow Jones average from the low in the second year to the high in the third year has been 45%. A Fed pivot could be the catalyst for additional gains into 2023.

The risk to that optimistic scenario and sustainable equity market gains for 2023 is that the inflation slowdown could be "transitory."

Suppose that the Fed raises official rates by 50 basis points at the December 13-14 meeting and follows that with another 50 basis points hike in early 2023. That would lift the federal funds rate to 5%. And if core inflation continues to run at 0.3% for the next five months, the twelve-month reading on core inflation in March 2023 would be 5.25%.

What are the odds of the Fed beating the current inflation cycle and bringing core inflation back to the 2% target with nominal rates below the inflation rate? History would say the odds may not be zero, but they are low. Official rates of 300 to 500 basis points above-reported core inflation broke the inflation cycles of the 1980s and 1990s.

Here are three reasons why the slowdown in inflation could prove to be "transitory."

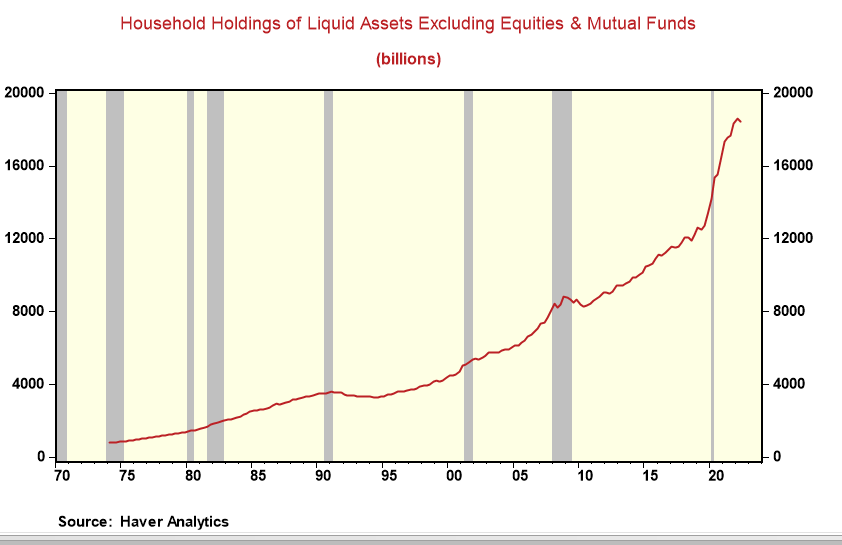

First, individuals are sitting on a cash bundle. At the end of Q2, households had $18.5 trillion in checking accounts, time deposits, and money market funds, equalling approximately 25% of total liquid financial assets, the highest share since the financial crisis. A Fed pivot could easily trigger a big risk-on rally in equity markets ("FOMO," fear of missing out, has not been retired), with spillover effects in the real economy. A rebound in equity prices, lifting consumer wealth, would boost consumer sentiment and trigger more robust consumer spending.

Second, the Fed rate hikes have hit the housing market hard. Home sales and new construction has slowed a lot in the past year. Yet, the number of existing homes for sale at 1.2 million in October is low and well below the level before the pandemic. The cost of mortgage borrowing, currently around 6% +, might look high nowadays, but that could change quickly in a risk-on environment when people's price expectations for housing starts to rise against a very low inventory backdrop. A more robust housing market would increase demand for commodities and consumer goods, lifting prices. And it has been the recent decline in consumer goods prices that have been responsible for the slowdown in core inflation.

Third, labor markets remain tight, with an unemployment rate of sub-4% and almost twice as many job openings as the number of unemployed. The jobless rate increased by over 200 basis points and remained relatively high for a few years following the tightening cycles of the late 1980s and 1990s. That helped sustain the slowdown in core inflation. Continued tightness in the labor markets is the biggest hurdle to achieving a sustainable slowdown in inflation as it maintains wage-cost pressures.

Policymakers will soon face Yogi Berra's "fork in the road." Will policymakers turn left (pause) or right (continuation of rate hikes)? Investors are betting on a left turn, expecting a rally in the short run. A right turn would create more pain in the short run but offer a better path for sustainable long-term gains.

Comments