Peak Inflation Is Hollow: It Provides No Context To Reduction in Speed or Duration of Cycle

- Joe Carson

- Jun 7, 2022

- 2 min read

Peak inflation is not a meaningful statistic. In some ways, it is similar to peak growth or peak earnings. Indeed, it provides no context to the reduction in speed or the duration of the cycle. It is hollow. The Fed made a mistake in thinking that the spike in inflation was supply-side driven and, therefore, temporary. It would be equally wrong to conclude that peak inflation signals a quick end to the inflation cycle.

There is a lot of talk of peak inflation as it somehow creates the impression that with inflation coming off its highs, the Federal Reserve has less need to tighten. Yet, peak inflation implies inherent linearity to inflation, which is not the case. Inflation cycles are non-linear. To be sure, inflation cycles rotate, move up and down, and broaden over time.

The thinking behind peak inflation is similar to the supply-side driven view of the current inflation cycle. Supply-driven inflation, according to some, is temporary as it will fall on its own accord once the unique factors disappear or dissipate in intensity. Yet, the error in that analysis is that it overlooks or ignores the spreading effect of inflation. In other words, as certain costs rise, it forces different prices up over time.

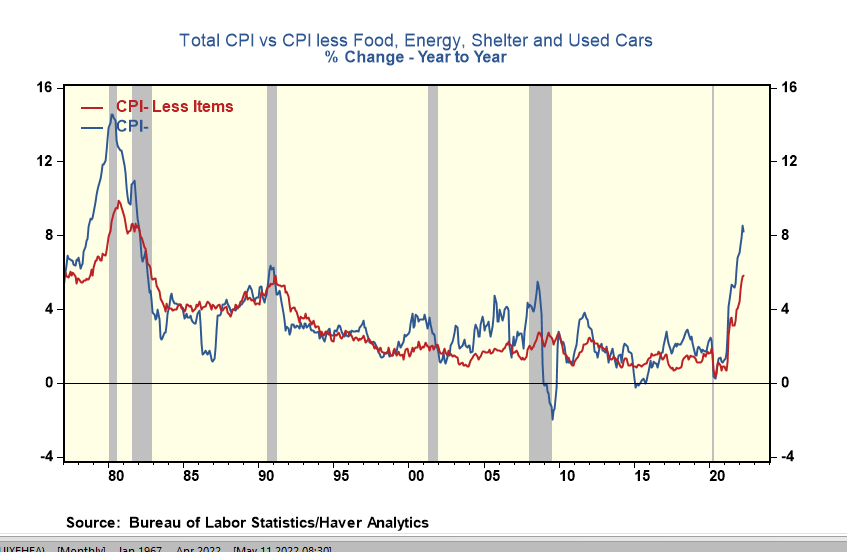

For example, in the 1970s, supply shocks (food and energy) played a massive role in starting the inflation cycle. After that, however, the inflation process spread, and for more than a year, inflation measures without food and energy costs were rising faster than those that included them.

A similar script is starting to play out today. For example, consumer price inflation has accelerated by 400 basis points in the past twelve months. Unique factors, such as energy +30%, used cars +23%, and food +9%, accounted for a lot of the spike. Yet, prices other than food, energy, shelter, and used cars accelerated by 330 basis points, rising 5.8%, the most significant acceleration and fastest increase in this broad price index in over 40 years.

Prices paid indexes are relatively high (low to mid 80%) for manufacturers and non-manufacturers in the May survey from the Institute of Supply Management, and wage costs for the rank and file posted their most significant monthly increase (0.6%) of 2022 in May. So as long as companies are saying costs for materials are increasing and workers' pay is as well, the Fed must conclude the inflation cycle lives on and ignore talk of peak inflation.

Something happened in 1971 alright, the beginning of fiat currency and odious debt.

hint: Nixon shock