Mr. Magoo's Bull Market: Investors Pay More For Growth & Worry Less About Debt

- Joe Carson

- Dec 8, 2020

- 3 min read

Updated: Dec 9, 2020

The world of finance changed in 2020. Investors nowadays are willing to pay more for growth and worry less about debt. Changes in investment philosophy and practices are directly related to the actions of the Federal Reserve.

Fed policies of near-zero official rates, buying record amounts of government and corporate debt, and the promise of no rate increases for an indefinite period has created an investor mindset of endless gains and little risk.

Decades of investing rules and practices are not repealed and remade in a single year. The unusual events and outcomes in the world of finance in 2020 create new tipping points. Mr. Magoo’s Bull Market is not sustainable.

Changes In Finance---Equities

The equity market had a lot of firsts in 2020. The S&P 500 will register a double-digit gain during a recession year. That might not sound like a big deal, but it is.

During the recession year of 2008 the S&P 500 posted a 38.5% decline; in 2001 equity prices fell 13%, and in 1990 equities dropped 6.6%.

Another first is the record high valuation of equities relative to nominal GDP. At the end of Q2, the ratio of the market valuation of domestic equities to Nominal GDP topped 2X times, a record high for the post-war period, exceeding the prior record of 1.9X times during the tech bubble.

At current market levels, the S&P 500 price-to-earnings ratio stands at 30, a record high. And that's before Tesla, which has a P/E ratio over 1200, is added to the S&P 500 index. Press reports indicate that the addition of Tesla would lift the P/E multiple by several percentage points.

The historic average P/E ratio is around 15X times. In other words, investors were paying for 15 years of annual profits. An average economic growth cycle runs about 60 months or 5 years. So in the past investors were willing to pay for three growth cycles, but today they are so confident they are paying for 6.

Changes In Finance---Debt

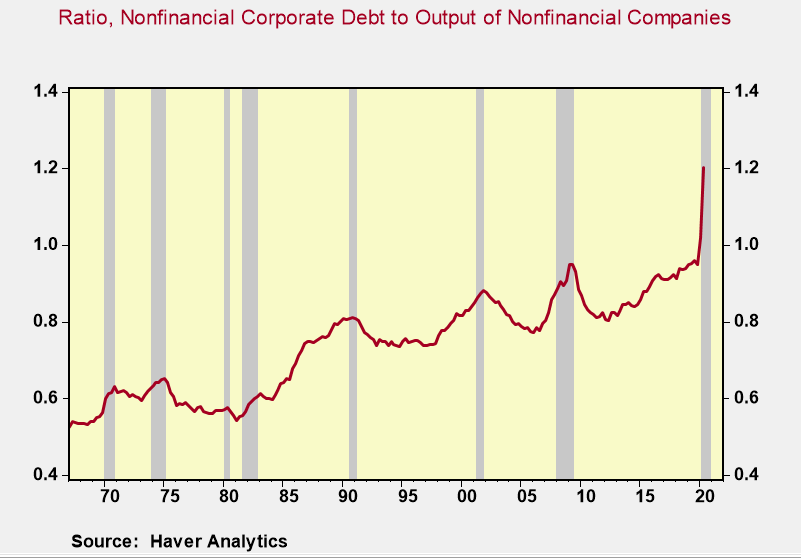

The debt markets had a lot of firsts in 2020. Businesses added to outstanding debt levels instead of paying down debt as have been the common practice during past recessions. Based on market data, non-financial corporate debt has increased by more than $1 trillion during 2020, lifting the outstanding level to more than $11 trillion.

At the end of Q2, the ratio of nonfinancial debt and loans to the nominal output of nonfinancial corporate businesses stood at 1.2X times. That's a record high, and 25 percentage points higher than the worse levels of the Great Financial Recession.

Nonetheless, investors seem to be unfazed by record debt levels. The average yield on investment-grade corporate debt currently stands at 1.85%, a record low.

The level of debt to earnings and cash flow used to be an important investment metric. Nowadays the burden of debt is looked at mainly through the lens of servicing it (i.e. interest payments) instead of paying it. While it is true low-interest rates reduce debt-servicing costs it does not lower the debt burden or eliminate the risks of high debt levels.

Investors act like the investment protocol of 2020 represents permanent change. The contrarian in me tells me it's not. Mr. Magoo's Bull Market is not sustainable and the big risk is that policymakers use the events and outcomes of 2020 to justify more government involvement in finance thereby creating new tipping points for the economy.

Comments