Investors Beware: Decades-High Profit Margins Will Fall Hard As Inflation Cycle Ends

- Joe Carson

- Apr 11, 2022

- 2 min read

Updated: Apr 12, 2022

Investors should brace for a sharp drop in nonfinancial companies' profit margins as the Federal Reserve raises official rates and shrinks its balance sheet significantly to reduce inflation. History shows that the unwind of inflation cycles tends to trigger an abrupt and sharp adjustment in margins as prices fail to cover overall costs.

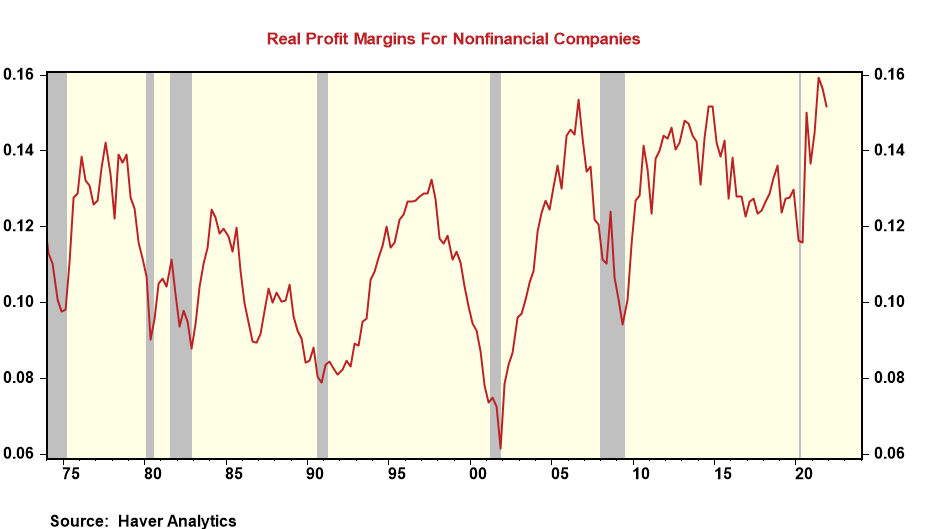

According to the GDP data, real profits margins of 15.3% in 2021 for nonfinancial companies were the highest since the mid-1960s. The significant increase in profits margins, up 2.3 percentage points over the prior year, shows that firms passed their higher costs for materials, supplies, and labor to the end customer. Yet, the inflation cycle's flip side shows that margins get squeezed.

The last time the Fed faced an inflation cycle as large as the current one and expressed an explicit commitment to reduce it and achieve price stability was in the early 1980s (the Volcker war on inflation era).

On the surface, today's inflation rate looks less threatening than that of the early 1980s. The current one is more than a year old, while that of the early 1980s was a spillover from the high inflation rates of the late 1970s. Yet, if measured using the same methodology of the early 1980s, today's consumer price inflation rate is as high. Meanwhile, the producer prices for all three processing stages, finished, intermediate, and crude, are significantly higher.

So what matters more for reversing an inflation cycle; the length of the price cycle or the scale and breadth? Policymakers should presume all three matter, and it will take a significant increase in policy rates and luck to break the current cycle.

Price cycles are uneven on the way up and equally, if not more so when the process reverses. Policymakers' projection of a miraculous slowing in inflation to its 2% price target (i.e., roughly a 600 basis drop in the reported consumer price inflation rate) and without triggering destabilizing effects in the economy and labor markets is not credible.

Significant and sharp drops in inflation rates trigger sharp declines in operating profit margins as firms' consolidated costs do not fall as quickly. For example, in the early 1980s, operating profits margins contracted by 400 basis points, and other periods showed even more significant margins decline.

The reversal in the current inflation cycle will not require as big of a policy adjustment as in the early 1980s. Still, the counter to that is that the labor markets are much tighter, limiting how quickly the firms can control their overall consolidated cost structure. As a result, it would not be a surprise that at the end of this process, firms operating profits experienced a decline equal to that of the early 1980s.

Comments