The "Income" Consequences of the Fed's Inflation Fight: The Main Reason Recession Risks Are High

- Joe Carson

- Jun 28, 2022

- 2 min read

Recession risks are high, in my view, because of the "income" consequences of the Fed's inflation fight. The math is very straightforward: A significant reduction in price inflation means less nominal revenue or sales, weak or negative operating profits, and less labor income. Consequently, the subsequent drop in national income growth would be sharp, rivaling some of the most significant declines on record.

The Fed aims to bring consumer price inflation back to 2%, down from the current rate of over 8%, a drop of 600 basis points. Slicing 600 basis points off the headline and roughly 400 basis points from the current reading of the core index would cause an uneven distribution of price changes, with prices for many consumer goods posting significant declines.

Commodities or consumer goods prices rose 10% in 2021. Given the stickiness in service sector prices, inflation for consumer goods would have to show no change or decline a few hundred basis points if the Fed successfully gets overall core prices back to a 2% rate. That would result in a sharp fall in revenue growth for a vast part of the retail sector.

Yet, the consumer price inflation fall would extend much further. Producer prices for finished goods and intermediate materials are cyclically aligned with consumer prices but are much more volatile. In 2021, producer prices for core materials and supplies rose 23%, 4x the core consumer price index and the most significant increase since the mid-1970s. If the Fed kills consumer price inflation, a record deceleration in prices for materials and supplies is in store.

The most significant reversal in materials prices occurred during the Great Financial Recession. In mid-2008, these prices were up 12% and one year later off 8%. If material price inflation drops to zero by early next year, it will exceed the price deceleration of 2008-09. As a result, the revenue drop for the materials producers would be substantial, crushing profits.

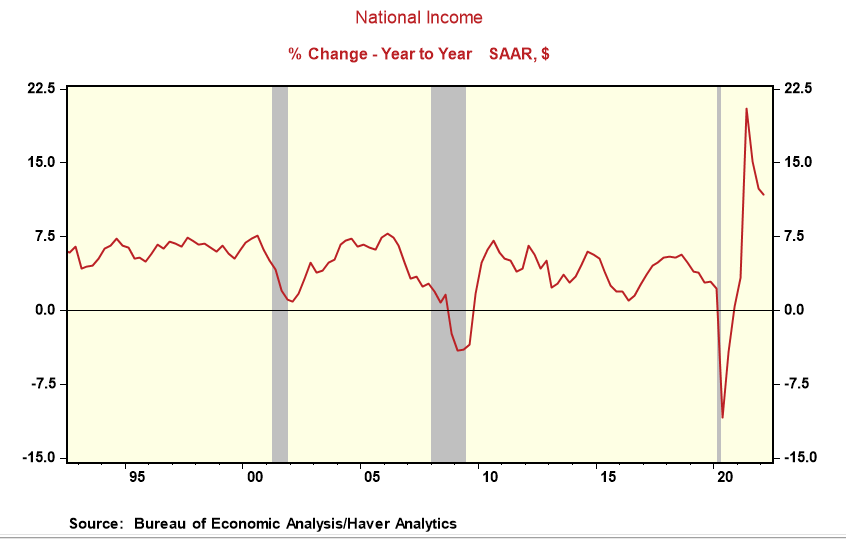

In 2021, with significant and broad consumer and producer inflation along with large wage gains, national income, 80% of which is accounted for by operating profits and employee compensation, rose 12%, 200 basis points faster than GDP.

If the Fed takes three-fourths of consumer price inflation out of the economy and all of the producer price inflation, the drop in nominal income would be sharp, especially when the hit to labor occurs.

Aggregate income would rise marginally, no more than 4%, and down from the current rate of 11%. That 700 basis points deceleration of nominal income growth would match the drop during the Great Financial Recession. Yet, in this case, it would still be marginally positive. Depending on how quickly firms cut back on labor and other costs, the fall in operating profits would be sharp, off at least 20%.

The Fed's inflation fight is in its early innings, and the biggest hit to company revenues, profits, and margins is months or even quarters away. Still, the process has started with reports of cuts in advertising and hiring freezes.

Comments