Asset Bubbles: The Danger of Anchoring Reported Inflation To A Non-Market Price

- Joe Carson

- Apr 20, 2021

- 3 min read

A non-market price---implied rents for owner-occupied housing.--- acts as an anchor for reported consumer price inflation. Does that mean policymakers will be right in that the uptick in consumer price inflation emanating from monetary and fiscal policies will prove to be "transitory"? Yes, it does, but that does not mean the economic and financial outcomes will be benign.

There are significant adverse consequences and dangers of relying on a non-market price to anchor reported inflation. Policymakers end up setting official rates too low, allowing real estate and equity values to trade at higher valuations than underlying fundamentals would otherwise support.

It is not a coincidence that two asset bubbles occurred in the past two decades when reported price inflation has been anchored by a non-market price. Is the third bubble in train?

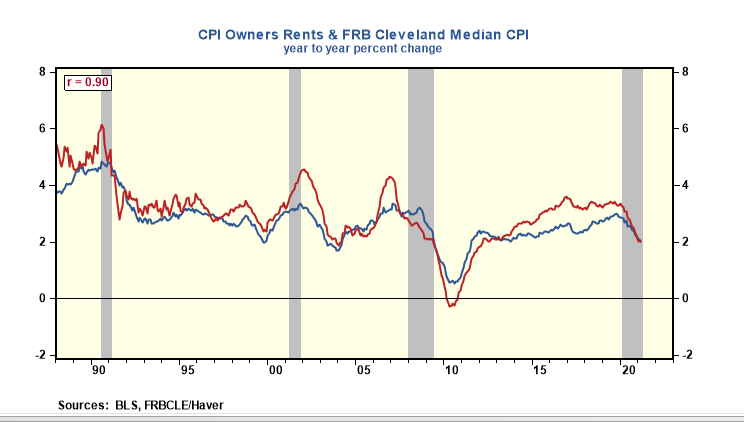

Non-Market Anchor In Reported Consumer Inflation

Following the consumer price index (CPI) release, the Federal Reserve Bank of Cleveland (FRBC) publishes a median consumer price index. The FRBC press release says, "The median CPI excludes all price changes except for the one in the center of the distribution of price changes, where the price changes are ranked from the lowest to the highest (or most negative to the most positive).

FRBC also argues that the median CPI provides a more accurate assessment of underlying inflation than the overall CPI and is "even better forecasting personal consumption inflation" (the Fed's preferred inflation measure) in the short-run and the long term.

Yet, decades of data show that the median CPI mainly tracks a single component--the non-market owners-rent--- of the CPI. The correlation between the median CPI and the owners-rents index is 90%. Medical services are the only other component of the CPI with a correlation value of over 50%, but its weight of 7% is relatively tiny compared to the 24% weight of owner-rent.

The relatively high correlation of owners' rent to median or core inflation is significant for two reasons. First, the anchoring process means that core or median CPI inflation cannot deviate from the non-market owners' rent price trends for very long. The non-market owners' rent is very stable month-to- month and year-to-year, increasing on average between 2% and 3, unlike market housing prices which can rise or fall at double-digit rates. Second, the owners' rent index exhibits non-cyclical behavior. That means the owner's rent price index will act as a counterweight to the cyclical price increases that result from the stimulative monetary and fiscal policies and pent-up demand from the pandemic.

The latter point is significant. That's because dampening or camouflaging actual inflation creates a false picture which, in turn, compels policymakers to maintain a lower official interest rate than what otherwise would be the case.

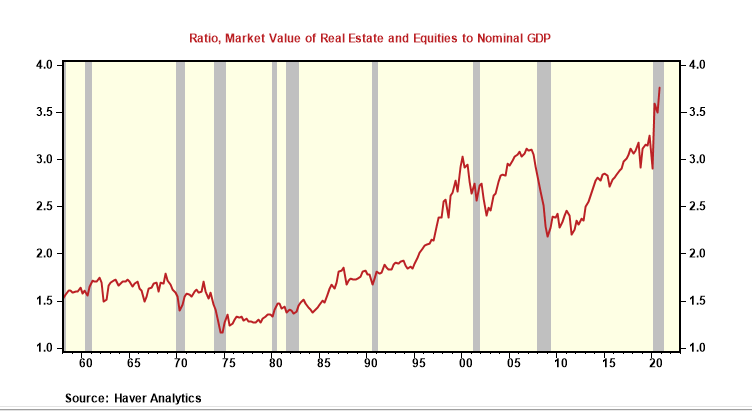

One of the consequences or dangers of linking the stance of monetary policy to a non-market-driven inflation rate is that it can lead to an escalation of asset prices that fundamentals alone don't justify.

Since the late 1990s, the ratio market value of the residential real estate and domestic equities to Nominal GDP ranged between 2.5x and 3.75x times, nearly twice the level that existed in the prior 50 years. The tipping points for the tech and housing bubbles occurred at a ratio of 3x times. At the end of 2020, the ratio stood at 3.75x times, a new record.

In the late 1990s, the Bureau of Labor Statistics stopped using the price signal from the single-family housing market to estimate the owner's rent.

That statistical change resulted in owners's rent being less of a market-based indicator. And since 2012, monetary policy has been using a 2% consumer price inflation rate as one, if not the main one, of the critical factors in determining the official rate policy.

Is it a mere coincidence that asset valuations relative to GDP have soared in the past two decades, and even more so after policymakers directly linked monetary policy to reported inflation, or is there cause and effect?

Federal Reserve Chairman Jerome Powell recently stated, "When something happened twice, it really time to go ahead and fix it." Not only did policymakers not fix monetary policy after the two asset bubbles, but they went in the wrong direction as it now directly links official rates to a non-market anchored inflation rate.

I would argue that the odds of a third bubble is relatively high for the simple reason monetary policy is more bubble-friendly nowadays, given the direct link between policy rates and non-market anchored inflation.

Comments